Nearly two years after the Reserve Bank of India (RBI) tightened regulations governing India’s peer-to-peer (P2P) lending industry, fresh questions are emerging around the sales practices and investment products being marketed by Transactree Technologies Pvt Ltd, the parent company of P2P lending platform Lendbox and alternative investment platform Per Annum.

The P2P lending platform is backed by investors like IvyCap Venture Advisors and Orios Venture Partners, among others, having cumulatively raised a total funding of $3Mn.

Multiple investors and prospective customers who engaged with Per Annum told Inc42 that company representatives pitched investment opportunities carrying unusually high returns while portraying the risks as limited.

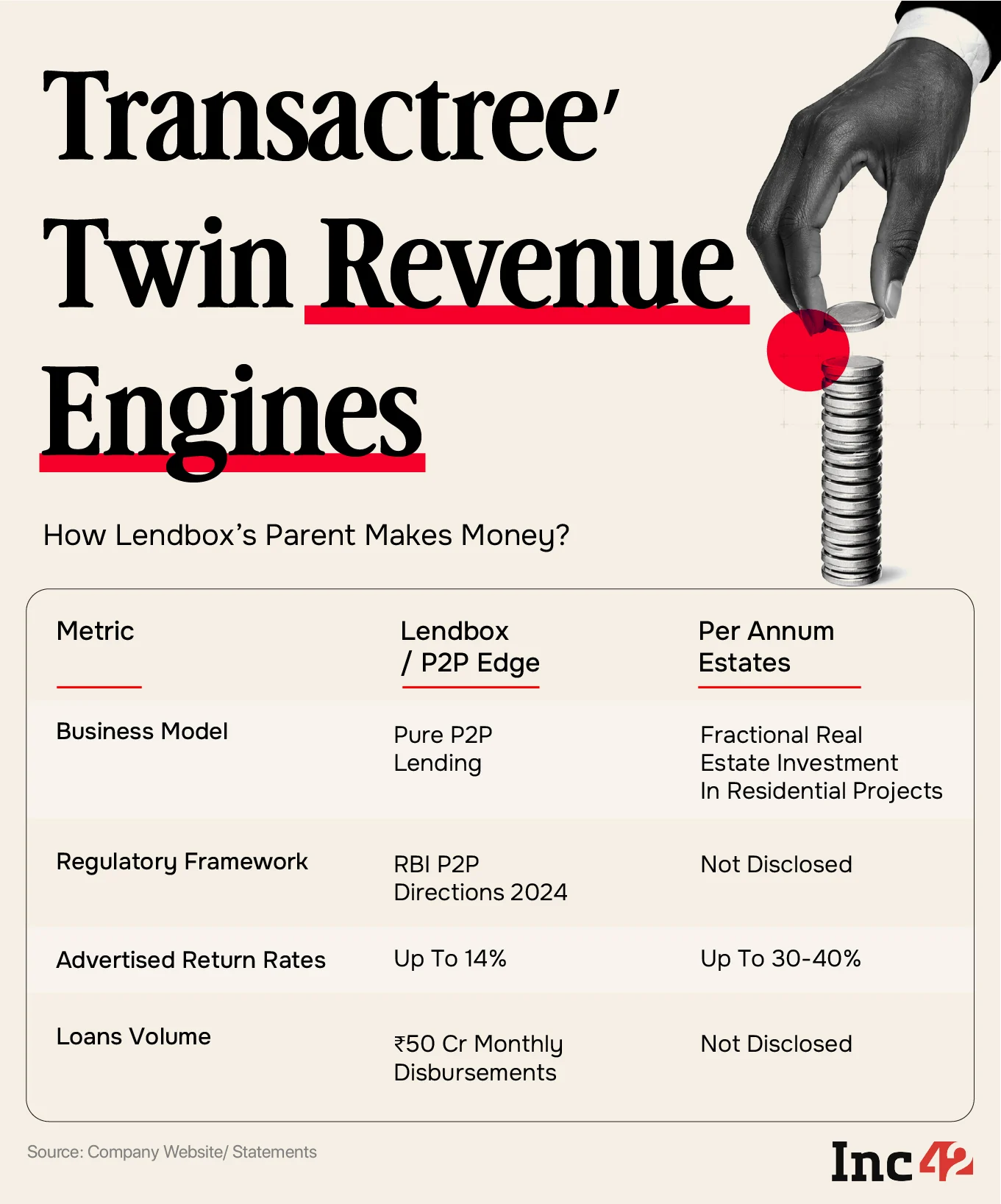

The products included P2P lending opportunities offering returns of up to 14-15% and fractional real estate investments that sales representatives claimed could generate returns of 30-40%.

Inc42 reviewed sales call recordings, investor communications and marketing materials shared by investors. In several interactions, sales representatives appeared to describe borrower interest spreads and platform structures as mechanisms that could absorb defaults and protect investor returns.

The claims raise an important question: are some of the very practices the RBI sought to eliminate from India’s P2P lending ecosystem re-emerging through new product structures and sales narratives?

The MobiKwik Connection

The issue assumes added significance because Transactree and Lendbox were previously linked to the MobiKwik Xtra controversy. While the company has maintained that regulatory changes affected operations and product functioning, investors who experienced difficulties withdrawing funds after the RBI’s 2024 regulatory overhaul continue to pursue legal remedies and complaints against the firms.

Against that backdrop, the emergence of new investment products and marketing claims has once again placed the spotlight on the company’s business practices.

The materials reviewed suggest that Per Annum is positioning itself as a platform offering access to alternative investment opportunities across credit and real estate.

The key question is whether investors are being adequately informed about the underlying risks, liquidity constraints and default exposure associated with such products.

Transactree Technologies Pvt Ltd said in a statement to Inc42 that following the RBI’s revised P2P framework the platform’s active lenders, borrowers, and live portfolio are below pre-regulatory levels.

“However, the platform remains active, facilitating approximately ₹50 Cr of monthly disbursements across 17,200 loans. With increasing participation from existing investors and continued inflow of new investors, we expect this run rate to reach approximately ₹100 Cr by the end of the next quarter, while maintaining a prudent and fully compliant approach to growth,” the company said in an emailed statement.

The questions surrounding Per Annum are inevitably linked with Mobikwik Xtra.

Mobikwik Xtra, built through a partnership involving Lendbox and fintech major Mobikwik, attracted retail investors by offering returns significantly above traditional savings instruments.

Many investors later alleged that the product had been marketed in a manner that created expectations of easy liquidity and predictable returns. However, following the RBI’s tightening of P2P regulations in 2024, numerous investors found themselves unable to access funds in the manner they had anticipated.

The controversy exposed a fundamental challenge within the P2P lending model.

Unlike bank deposits, loans are inherently illiquid assets.

Investors can generally recover funds only through borrower repayments or by finding another lender willing to assume the exposure. When underlying loans face delays or defaults, liquidity can evaporate quickly.

The episode triggered legal complaints, police complaints and significant investor backlash.

While the company has consistently maintained that regulatory changes materially impacted product operations, the episode highlighted broader concerns regarding risk disclosure, liquidity expectations and the marketing of alternative credit products to retail investors.

Yet even as Lendbox continued dealing with the aftermath of Mobikwik Xtra, Transactree expanded its consumer-facing investment Per Annum.

Old Products In A New Wrapper?

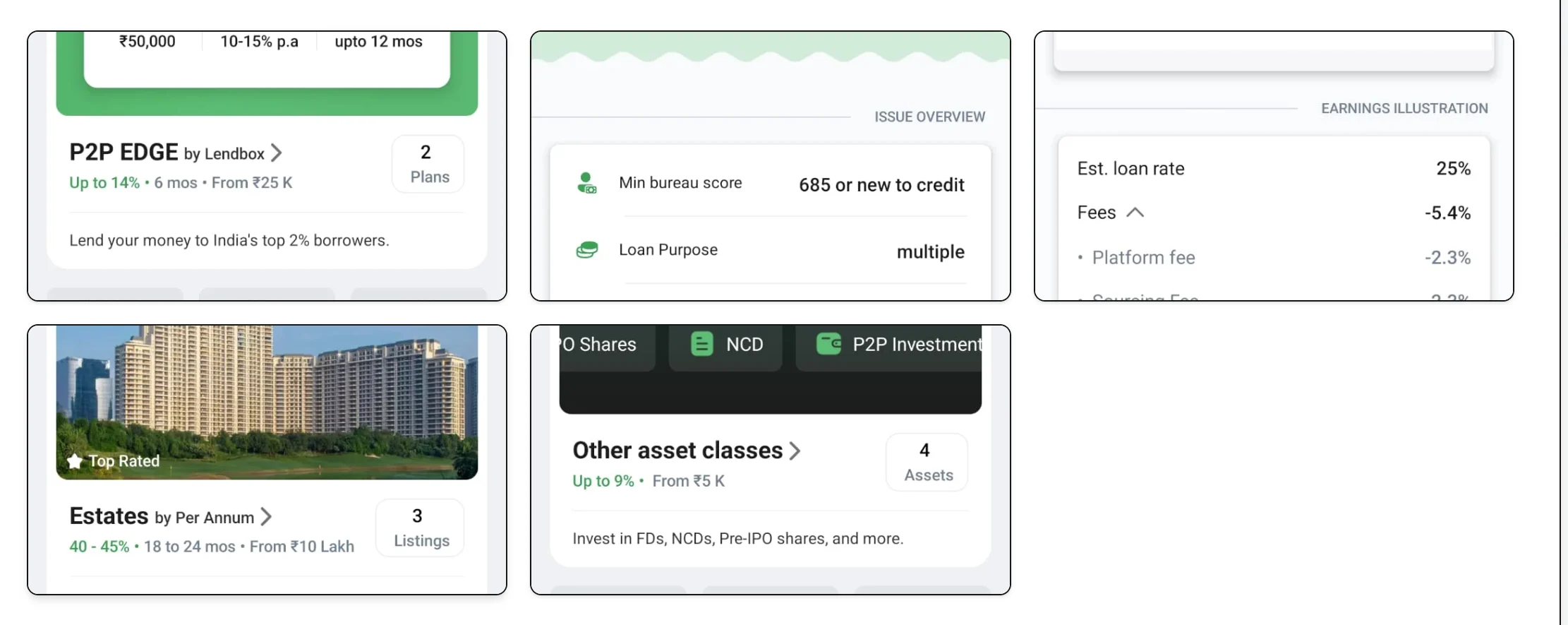

Per Annum’s product suite includes two primary offerings.

The first is “Estates,” described as a fractional real estate platform giving investors access to premium residential projects in Gurgaon, Bangalore and Mumbai, with entry points of ₹5–10 Lakh for properties that “traditionally cost ₹2–11 Cr.”

Investors are promised “capital appreciation of prime real estate markets” and “complete end-to-end management of the process” from acquisition to exit with full transparency.

The second is “P2P Edge” — peer-to-peer lending facilitated by what Per Annum describes as “a decade-old, RBI-licensed NBFC-P2P partner.

While Per Annum’s own app interface lists P2P Edge as offering “up to 15%” returns over a six-month tenure with a minimum bureau credit score requirement of 685, marketed under the line “lend your money to India’s top 2% borrowers.”

Inc42 reviewed several sales pitch calls of Per Annum representatives and the investors which suggest that the company continues to prime “assured returns” to the lenders with the loans being disbursed at 25-30% interest rates that act as buffer against defaults in repayments of some borrowers.

The representatives also pitched the Estates product at a return of 38 to 40%, and referenced an upcoming Non-Convertible Debenture product carrying a fixed 11.5% monthly payout.

That description of a margin engineered to “cover” defaults so that the lender never takes a loss is exactly the practice the RBI’s August 2024 Master Directions have prohibited.

The directions state that an NBFC-P2P “shall not provide or arrange any credit enhancement or credit guarantee,” and P2P loans under the framework are structured to be entirely unsecured, meaning any default is supposed to be borne by the lender, not absorbed by the platform.

The RBI’s 2024 guidelines also stated that P2P platforms cannot market their products with assured or minimum returns, cannot offer liquidity options that mimic deposits, and cannot present themselves as alternatives to bank fixed deposits.

However the company claims that under the updated framework, repayments align strictly with loan tenures and individual borrower repayments.

“Lenders are given a repayment schedule for each loan. Adequate disclaimers about the possibility of loss are provided wherever required. There are no assured liquidity or guaranteed return products. Lenders are given an approximate idea of how much they would earn net of defaults,” it added.

Furthermore, the Estates product adds another layer of complication.

Notably, fractional real estate investment in India sits outside the NBFC-P2P regulatory framework entirely.

Depending on how it is structured, whether the investment is in securities, in property rights, or in a collective vehicle, it could fall under SEBI’s purview, under RERA, or potentially in a regulatory grey zone that offers investors little formal protection.

The concern raised by investors is not necessarily that high-return products exist. Rather, it is whether consumers fully understand that these returns are linked to underlying credit risks, borrower defaults and liquidity constraints.

In response to our queries, the P2P lending firm stated, “Per Annum is a distributor for multiple alternate assets/wealth/ownership products and has partnered with different companies which manage these products. The specific structure, underlying assets, and risk disclosures vary by product and are governed by the respective product documentation. We do not offer any risk-sharing arrangements to lenders/investors under any product.”

Several fintech analysts say that investment products should not be presented in a manner that resembles guaranteed deposits unless such guarantees genuinely exist.

The RBI’s 2024 overhaul was intended to remove precisely these ambiguities.

Why The RBI Changed Rules

Understanding the significance of these claims requires understanding how India’s P2P industry evolved.

Peer-to-peer (P2P) lending was once pitched as one of Indian fintech’s most disruptive innovations. By directly connecting borrowers with lenders through technology platforms, the model promised to democratise credit and deliver double-digit returns to investors frustrated with traditional fixed-income products.

For years, the sector expanded rapidly, attracting retail investors with the prospect of earning 10-15% annual returns

Platforms highlighted data-driven underwriting, diversification and technology-enabled collections as tools that would minimise risk. The startups operating on this business model claimed to have an asset-light credit distribution model after acquiring RBI-mandated P2P-NBFC licenses.

Essentially, the fintechs were operating as loan distribution marketplaces with no capital deployed from their own books but from the retail investors.

Even as the overall sector raised a cumulative funding of $200Mn, VC funding players like Faircent, Lenden Club, Lendox, and Liquiloans claimed to manage thousands of crores as Assets Under Management (AUM).

But the optimism began to fade as defaults mounted, and concerns emerged around how some platforms marketed liquidity and returns and investors complained of losing money or stuck funds.

In 2024, the Reserve Bank of India tightened regulations governing P2P lending platforms, seeking to eliminate practices that blurred the distinction between marketplace lending and deposit-like products.

The regulator barred arrangements that could create the perception of guaranteed returns or instant liquidity while strengthening rules around fund transfers and platform operations.

The regulatory concern was that some of the P2P lending platforms had started acting like shadow banks, promising guaranteed returns, FD alternatives and marketing claims of unusually high returns.

The regulatory intervention had a significant impact. Industry participants say the overall P2P ecosystem shrank sharply after the new norms came into force, with weaker players struggling to adapt to the stricter framework and eventually having to shut down.

The overall AUM of the P2P lending industry reportedly shrank from ₹10,000 Cr to ₹3,000 Cr from 2023 to 2025.

The Mystery Of Lendbox’s AUM

Another question surrounding Transactree Technologies concerns the size of Lendbox’s business.

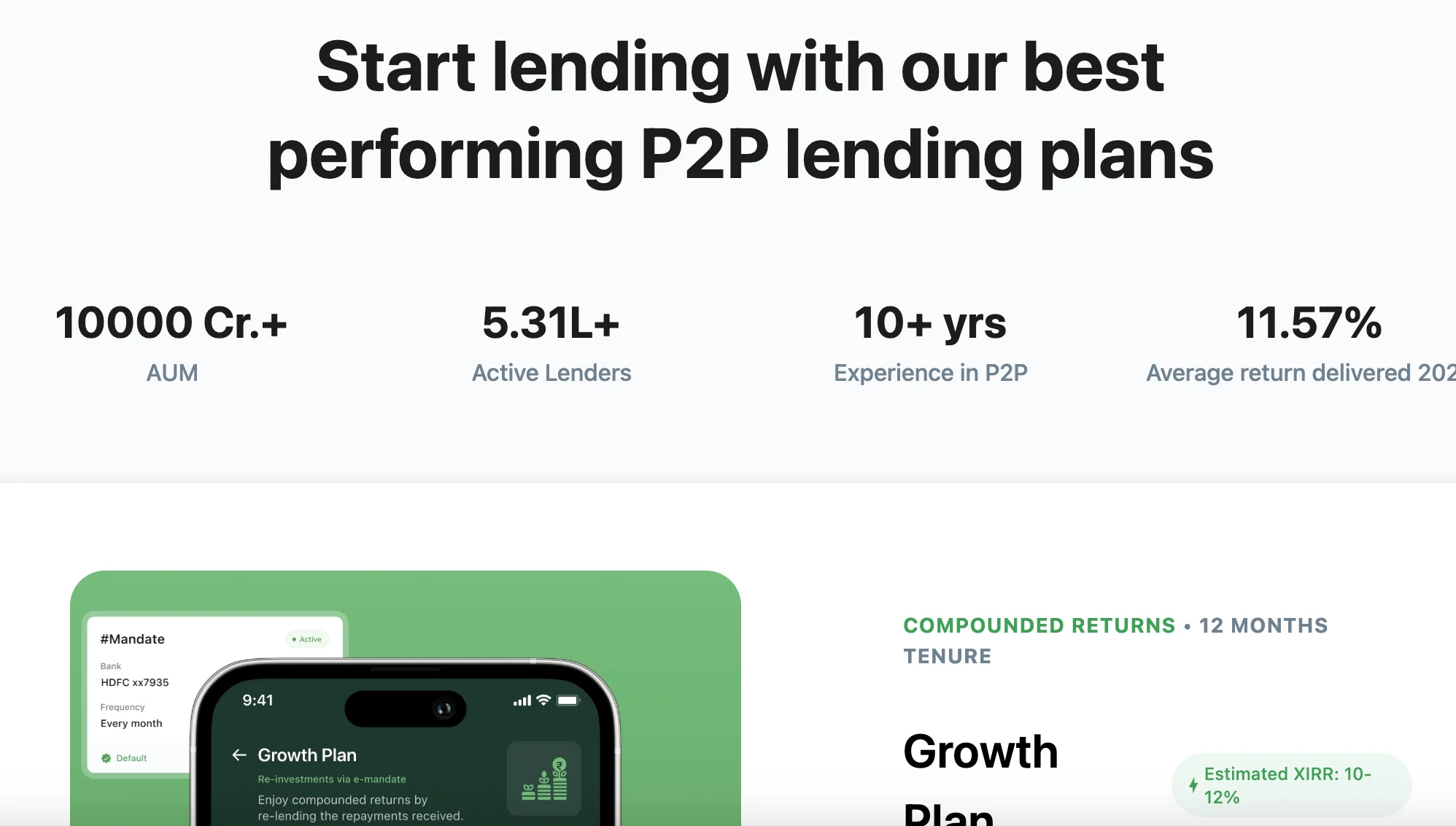

The platform continues to publicly highlight an assets under management (AUM) figure of approximately ₹10,000 Cr.

At first glance, the number suggests a dominant market position.

However, the claim appears difficult to reconcile with broader industry developments.

Meanwhile, Transactree Technologies denied any public reference to ₹10,000 Cr AUM. The figure might have been quoted in some particular context, such as disbursals or lender deposits over a certain period,” it added.

Market participants have indicated that the RBI’s 2024 regulatory changes significantly reduced the size of the organised P2P market. Industry estimates suggest that the overall live P2P book contracted sharply after the crackdown as platforms were forced to alter their operating models.

Adding to the puzzle is the position taken by rival platform LenDenClub. The company, which has been preparing for a potential public listing, has publicly indicated that it now commands a substantial share of India’s P2P market, with some estimates placing its market share between 70% and 80%.

If the overall industry has contracted materially and a single player occupies the majority of the market, how does Lendbox continue to report a ₹ 10,000 Cr AUM?

The answer may lie in definitions.

In financial services, AUM can refer to different metrics like cumulative loan originations or outstanding live assets.

Without a standardised disclosure, investors may not know whether the figure reflects currently active assets or cumulative lending conducted over several years.

A cumulative historical number can appear impressive while masking a much smaller live business or loan book.

The issue becomes even more relevant given persistent market discussions around asset quality.

The RBI, under the 2024 Master Directions guidelines of 2024, has strictly prohibited misselling of financial products in the P2P lending ecosystem, with specific reference to avoid use of phrases like minimum credit guarantees, providing explicit information of the credit risk and failure to provide credit data in the public domain.

To be sure, Lendbox and Per Annum’s parent company, Transactree Technologies, was fined a ₹40 Lakh penalty in May 2025 by the RBI, holding the company responsible of routing investor funds through an unauthorised co-lending escrow account — a mechanism that sits outside the prescribed fund transfer framework for P2P platforms.

The central bank had also pulled up fintech for failing to disclose credit assessments and risk profiles of borrowers to prospective lenders. The P2P lending platform had also disbursed loans to individuals without obtaining specific approvals from those individual lenders.

Industry executives and investors have repeatedly raised questions about borrower quality across several P2P platforms, arguing that the race to maintain growth often resulted in weaker underwriting standards.

A claim of an outsized AUM, opacity in the platform’s gross and net NPAs and the failure to reveal information on defaults or borrower information since the RBI crackdown raise serious questions about Lendbox and Per Annum’s current business model.

Financial Pressure And The Incentive to Find New Growth

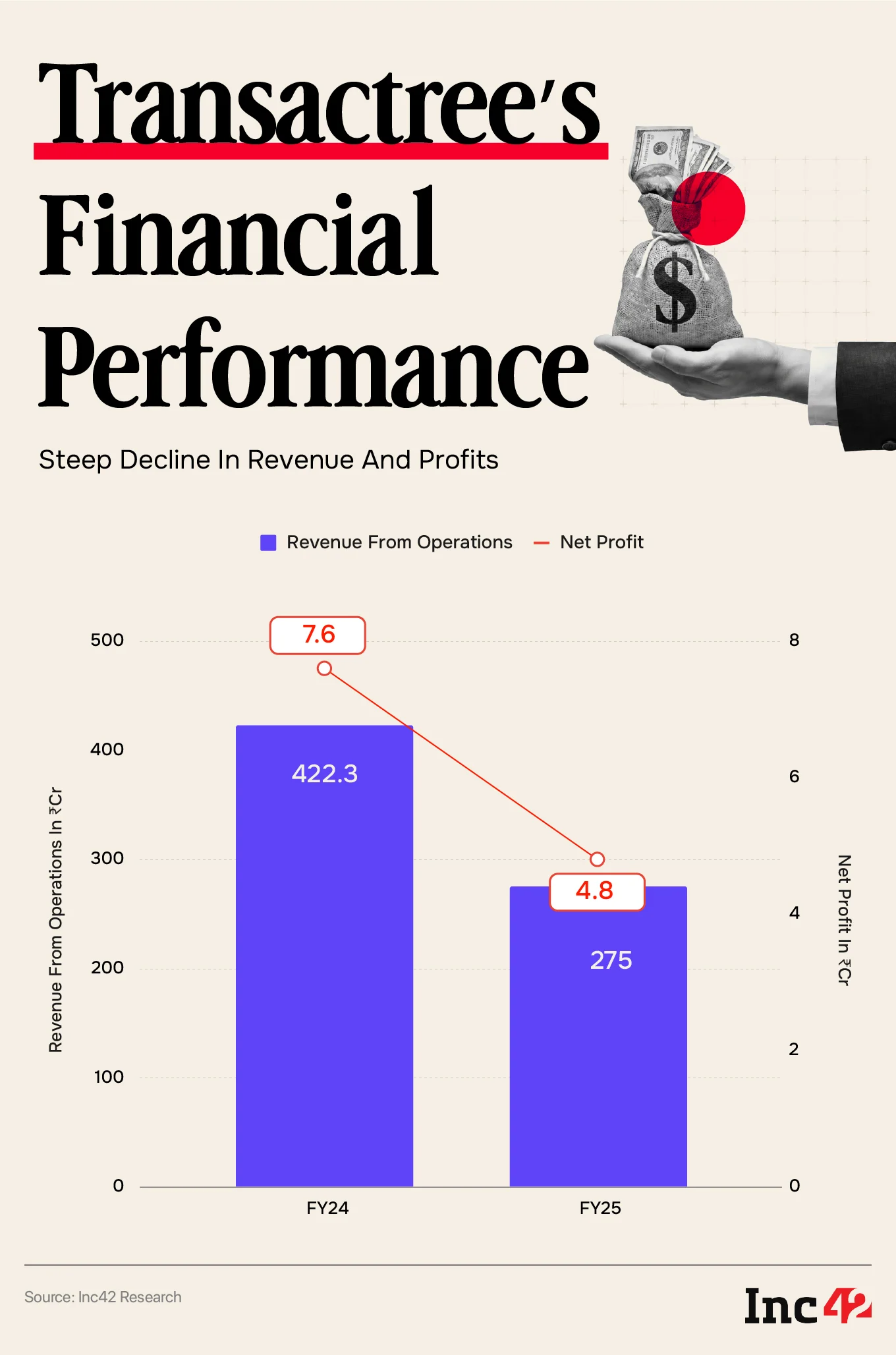

The financial statements of Transactree Technologies provide another important layer to the story. The company’s FY25 accounts indicate that revenue from operations declined from approximately ₹422.3 Cr in FY24 to around ₹275 Cr in FY25, a fall of nearly 35%.

Profit before tax also declined significantly, while net profits reduced from around ₹7.6 Cr to approximately ₹4.8 Cr.

The company also reported negative operating cash flows in FY25 despite remaining profitable on paper.

While the company came under the RBI’s scrutiny and faced police and legal complaints from the investors, the balance sheet shrank from ₹55.65 Cr in FY24 to ₹38.54 Cr in FY25.

The interest payable to investors fell from ₹16.08 Cr in FY24 to ₹4.50 Cr in FY25.

That decline in investor interest accruals is likely a signal in the reduction in AUM, or it could reflect payouts made to investors pressing for exits after the Mobikwik Xtra controversy.

Either way, the paltry investor interest of ₹4.50 Cr in FY25 ( as mentioned in the company financials) is not indicative of the ₹10,000 Cr AUM claim ( as mentioned by the company’s website).

According to its FY25 financials reviewed by Inc42, the company’s auditors have also noted several related party transactions to different entities by the name of Transactree Services Private Limited, and Transactree Enterprises Private Limited, were done without a formal agreement on repayment terms or interest — noting they were “unable to comment whether the terms and conditions of the aforesaid advance are prima facie prejudicial to the interest of the Company.

Transactree Private Technologies in response to our queries said that it provides lender sourcing for TTPL just like multiple other channel partners that work with the company.

While a weakening financial situation for Lendbox and Per Annum could be due to investor withdrawals and regulatory action, which cast an impact on the overall P2P industry, the startups’ foray into the ancillary businesses with outsized claims and investor challenges reveals that not all lessons have been learnt.

Several experts argue that Indian fintech has repeatedly encountered the same cycle under which a product category grows rapidly, attracting high returns and attracting investors.

Marketing and sales pitch highlight the technology stack and convenience until underlying risks become apparent and regulatory authorities intervene.

If investors now believe that similar risks are being presented through new wrappers as is the case with Per Annum, the next phase of oversight may have to focus not only on how products are structured, but also on how they are sold.

Until then, the unanswered questions surrounding Lendbox and Per Annum are likely to remain at the centre of a much larger debate about trust, transparency and the future of India’s alternative lending industry.

[Edited By Nikhil Subramaniam]

The post ₹10,000 Cr AUM, MobiKwik Xtra & Per Annum: Lendbox’s Risky Regulatory Dance appeared first on Inc42 Media.

Source link